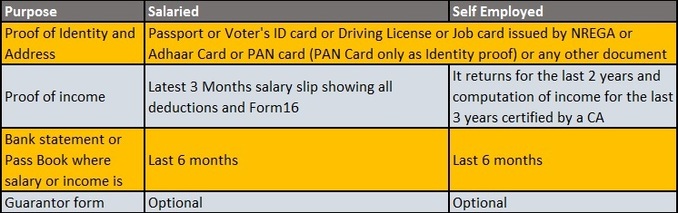

To avail a home loan in India is never an easy task. With rising cases of bad debts, banks are becoming increasingly wary about lending to anyone with whom even the slightest of risk is involved. While you can't change strict procedures followed by the banks, there are still some ways that can improve your chance of getting your loan approved without any hassles. Recently, three of the country's largest banks have reduced their lending rates by 0.15 percent to 0.25 percent, bringing lots of hopes among home-loan borrowers to pay less on their monthly EMIs. While State Bank of India and HDFC Bank cut their benchmark base rate by 15 basis points to 9.85% from 10%, ICICI Bank reduced its base rate by 25 basis points to 9.75%. If you're also planning to buy or invest in a residential property, consider these simple steps to avail a home loan faster: 1. Build your reserves: You should think 2-3 years in advance before planning to buy a house. Build your reserves and save a fixed amount every month so that you can pay maximum down payment at the time of availing a home loan. Banks usually provide loans for 75-85 per cent of the total value of the house, but one should strive to pay as much as possible in order to reduce the number of EMIs and the subsequent interest rates. It is advised to pay 40 per cent of the total value of the house as down payment and take loan for the remaining. The more amount you pay, better are the chances of you getting the loan approved from the bank. 2. Get co-borrowers: If your income isn't enough to get the required home loan or you're stretching it too much, there is an option of getting a co-borrower for your loan. This means that the liability of the loan will be shared between you and the co-borrower, and his/her income will also be taken into account by the bank to calculate the repaying power. Banks generally allow six co-borrowers for a home loan. Getting a co-borrower enables you to avail a bigger amount of loan as banks consider it less risky to lend to people with better income prospects. 3. Pay off your credit card bills: Banks take into consideration your credit card payment history and any other personal loans that you may have, before passing a new loan on your name. Ensure that you've cleared all your pending credit card payments and other personal loans before applying for a home loan. A well-maintained account history enables banks to forward your home loan application faster to the upper management. Try to clear all your outstanding payments few months before you apply for a home loan. 4. Maintain your bank account: When you apply for a home loan, the first thing that banks ask is at least six months of your bank account statement. Banks enquire about whether there are any discrepancies in your account in the form of a bounced cheque, an unpaid EMI or low balance at the end of each month. Banks consider it negative if you maintain a low balance at the end of every month as this would mean you are already stretching your monthly expenses and a home loan would put an additional burden on you. Tidy up your bank account, keep a healthy balance and pay all your EMIs on time, before you apply for a home loan. 5. Get all your documents in order: There are several documents required by banks prior to processing your home loan application. The documents include your identity proof, address proof, bank statements, proof of annual income and guarantor form, among others. Apart from these documents, banks also ask for application form duly signed by you, processing fee cheque, six cancelled cheques and an ECS mandate form. There are also property documents require such as copy of the allotment letter or buyer agreement and a receipt of payments made to the developer. If you've all these documents ready, there is hardly any reason that bank refuses to process your application. 6. Buy from a reputed builder: Banks do verify the property for which you want to avail a home loan. In cases when a home loan borrower couldn't be able to payback the loan amount, banks repose the property and recover the money by selling it again. It is for this reason, banks do a thorough check of the property, the builder and the location, so not to find any trouble in reselling it. It is therefore advised to buy property from reputed builders who take care of these concerns and often tie-up with banks for easier processing of your home loan application. Buying a property from a reputed builder also helps buyers to stay away from any property dispute or legal hurdles in future. Mr. Anil Mithas, Chairman & Managing Director at Unnati Fortune Group says, “With top banks reduced their interest rates on home loans, this is a great opportunity for people to buy their dream home. With lowered monthly EMIs and favorable economic environment, even middle-class families can afford to buy their own residential properties in India. The development will give a major boost to the real estate sector and helps in bringing positive sentiments back into the sector.” |

|

6/9/2015 09:14:08 am

Are you a business man or woman? Do you need funds to start up your own business? Do you need loan to settle your debt or pay off your bills or start a nice business? Do you need funds to finance your project? We Offers guaranteed loan services of any amount and to any part of the world for (Individuals, Companies, Realtor and Corporate Bodies) at our superb interest rate of 3%. For application and more information send replies to the following E-mail address: [email protected] 6/11/2015 08:30:33 pm

How Do I Get A Va Home Loan, How Can I Get A Home Loan, How To Get Home Loans and How To Get The Best, we are here to answers all your queries. Comments are closed.

|

Archives

May 2015

MR. ANIL MITHAS

Chairman & Managing Director at Unnati Fortune Holdings Ltd Categories |

RSS Feed

RSS Feed